Your credit score calculation is based on multiple factors, one being your credit utilization ratio. Understanding how your spending habits with your credit card can influence this ratio is important because credit utilization directly impacts your credit score. So, what exactly is credit card utilization, and why is it so important?

Understanding Credit Utilization

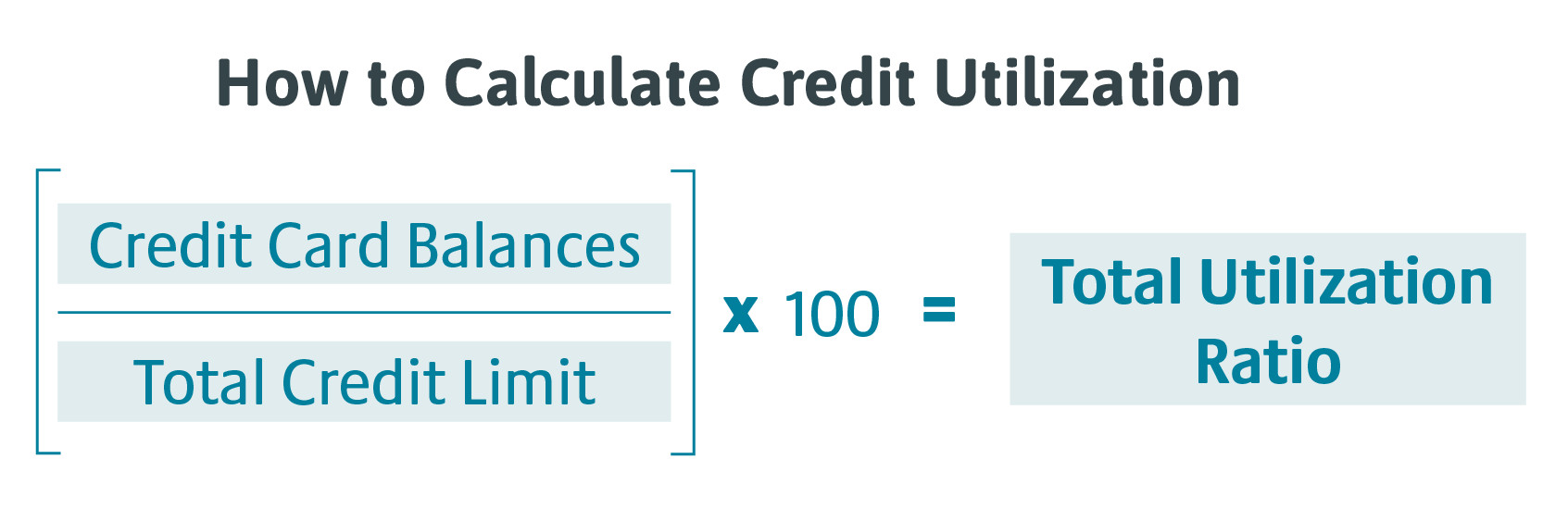

Credit utilization, also known as credit utilization ratio, refers to the percentage of your available credit that you’re currently using. It’s a key component of your credit score calculation and is calculated by dividing your total credit balances by your total credit limits and then multiplying by 100 to get a percentage.

For instance, if you have two cards with a $5,000 limit each and one has a $5,000 balance while the other sits at $0, your total utilization is 50%. It is important to note that your total credit utilization ratio includes all open credit cards.

Impacting Your Credit Score

Credit utilization is a crucial factor in determining your credit score, accounting for 30% of your FICO credit score and 20% of your VantageScore. Generally, the lower your credit utilization ratio, the better it is for your credit score.

Lenders and credit scoring models typically prefer to see a credit utilization ratio of 30% or lower. This demonstrates that you’re not overly reliant on credit and are managing your debts responsibly. Higher credit utilization ratios can indicate to lenders that you may be overextended financially, which can be seen as a red flag and potentially lower your credit score.

How to Manage Credit Card Utilization

Because your credit utilization is a large part of your credit score, it’s important to understand how to manage it effectively.

- Keep Balances Low: Aim to keep the balance on each credit card as low as possible.

- Pay Balances in Full: Whenever possible, pay your credit card balances in full each month to avoid carrying over balances and keeping your utilization rate low. You can also consider making payments on your credit card throughout the month to keep balances low.

- Request Credit Limit Increases: Requesting a credit limit increase from your card issuer can decrease your utilization ratio. Just be sure to not increase your spending with a higher credit card limit. If you are a Park View credit card holder, learn more about how to request an increase here.

- Use Multiple Cards Wisely: Distribute your expenses across multiple credit cards rather than maxing out a single card. For instance, if one card carries a $3,000 balance and another $2,000, that is preferred to a single card with a $5,000 balance.

- Open a New Line of Credit: Opening a new credit card or line of credit increases your overall available credit. Many cards, like the Park View Everyday Rewards + Card, offer introductory bonuses and other perks. However, opening several new credit card accounts in a short time can hurt your credit score.

While credit cards offer convenience and easy access to funds, it’s important to use your card wisely because it affects your credit utilization and, consequently, your credit score. By using your card responsibly, making informed decisions, managing your credit utilization effectively, you can not only enhance your credit score but also pave the way for a more secure financial future.

Share This

You May Also Like

Private vs. Federal Student Loans: What to Know Before Borrowing

Mid-Year Financial Checkup: Five Simple Steps to Strengthen Your Financial Health